Re-mortgaging is the process of switching your existing mortgage to a new deal. You can re-mortgage with the same lender often called a product switch or a let us shop around to find the deal that best suits your circumstances.

Think carefully before securing other debts against your home. Consolidating debt may reduce your outgoings now, however you may pay more interest over your mortgage term. Your home may be repossessed if you do not keep up repayments on your mortgage.

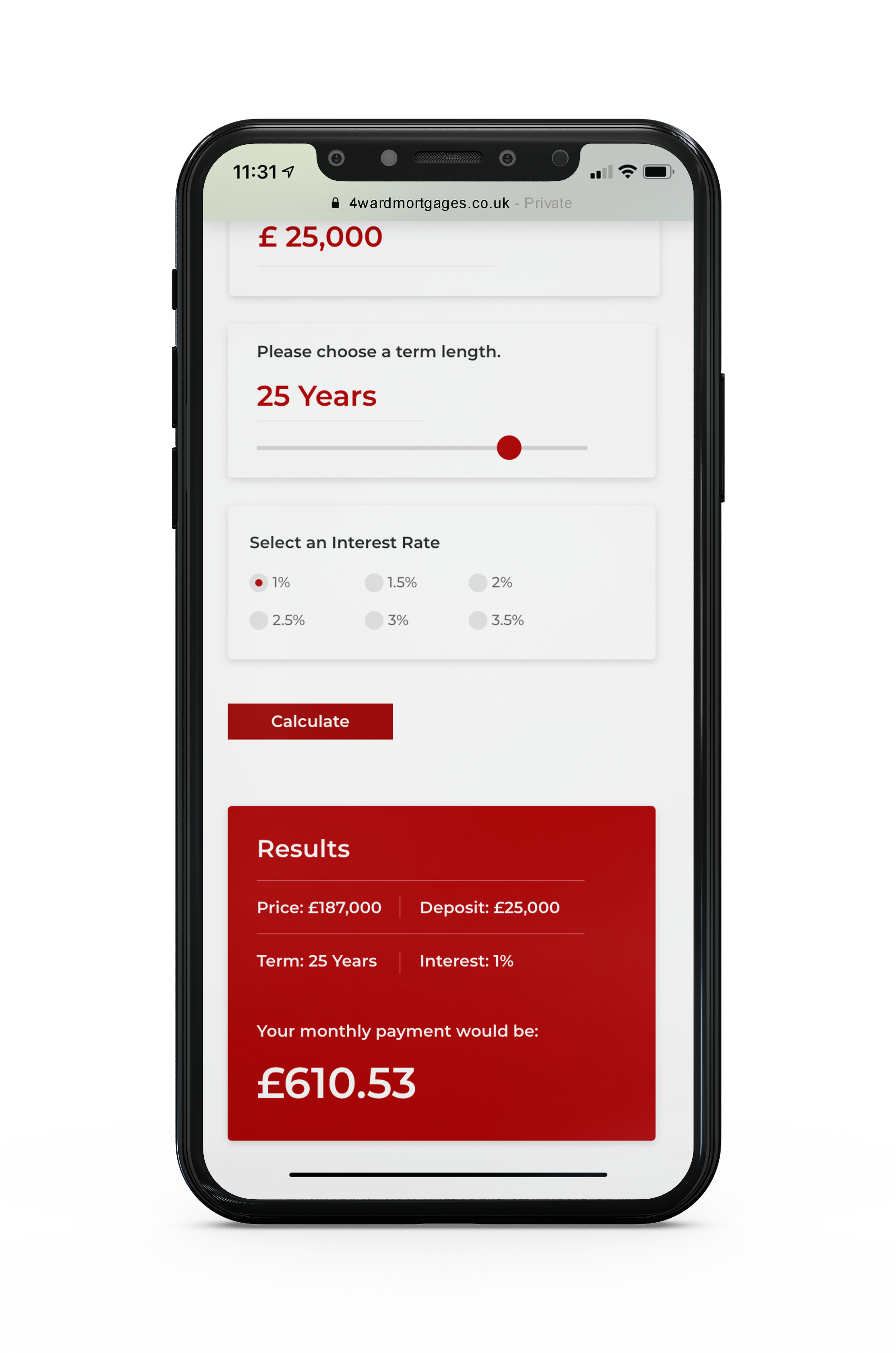

Try our monthly repayment calculator.

If you’re buying for the first time, you could be unsure as to what

a monthly mortgage payment should look like – use our calculator

to get a rough estimate.

Seeking a better rate: Your current deal could be coming to an end - most fixed-rate mortgages last between two to five years before they go onto the lenders standard variable rate. You may want to find better interest rates.

2

Raising additional funds: Some people re-mortgage their property to get access to a sum of money. You could potentially free up money to pay for home improvements, for example, or to pay off existing credit commitments.

3

You may want to find better interest rates. To find out how much you could save on your mortgage contact us on 07488 317183, email mark@4wardmortgages.co.uk, or book an appointment with us.

Frequently Asked Questions

Mortgages and protection can be confusing,

see the most commonly asked questions

and answers, to put your mind at rest.

Why life insurance is so important when you're a parent.

It goes without saying that raising children can be expensive, so your income, or that of another household member, is often the only way to pay for the everyday costs that come with looking after a child.

If you or someone you rely on were to pass away, it would take its toll financially, in addition to the emotional stress. Life insurance is one way to have a safety net in place.

Why life insurance is so important when you're moving home.

If you have life insurance, it’s a good idea to regularly review the cover to make sure it’s right for you and your current circumstances.

When you sign up for a policy, the extent of cover – how long it lasts, and how much it would pay out – is based on your financial situation and commitments at that time.

But these can change. Your life insurance policy needs to change as well to ensure your family is fully protected if the worst happens to you or your partner, so when moving home it’s important your cover still meets your needs.

Why life insurance is so important when taking out a new mortgage.

Mortgage life insurance can be used to help your loved ones pay off your mortgage if you die.

This type of life insurance is often sold as a decreasing-term policy so, as you gradually pay off your mortgage, your pay-out reduces over time. A mortgage life insurance claim typically pays out as a lump sum.

It’s designed to protect your loved ones if you die before your mortgage has been paid off. It will provide them with a lump sum so they can clear the mortgage debt and have one less financial burden at an already difficult time.