Contact us to work out how much you could afford to borrow, based on your income, regular spending and any debts you might have. Then once we have completed a fact find we will start the process of sourcing an Agreement in Principle to see if we can find a lender prepared to lend the amount you need. Once you have that, and you’ve found a property to buy, we will apply for the mortgage for you, this means you’ll talk to one of our mortgage advisers, who’ll recommend a mortgage tailored to you.

The lenders usually ask for minimum of 5 – 10% of the property value as a deposit – but some mortgages are designed to help if you’re struggling to save up that amount.

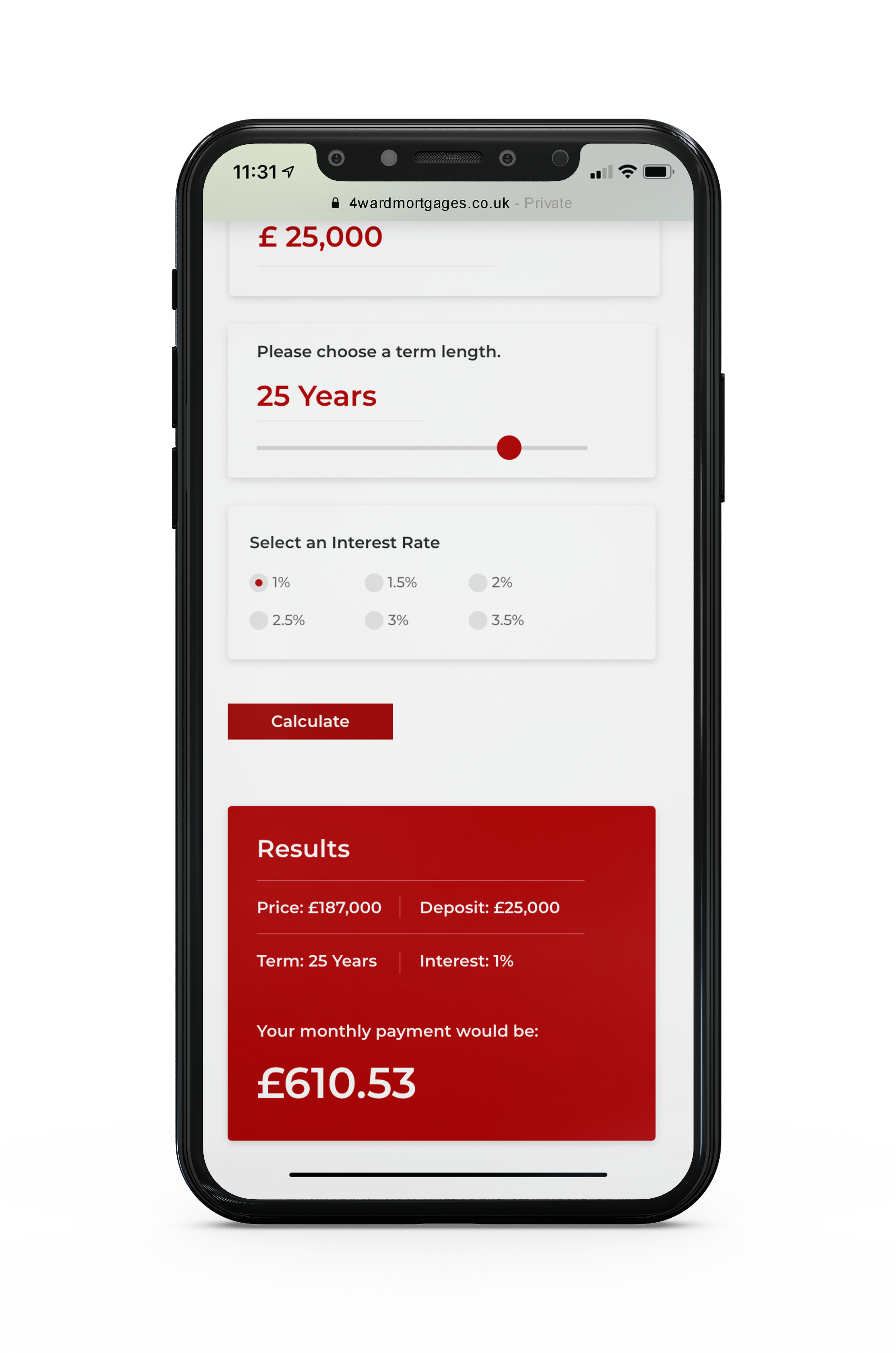

Try our monthly repayment calculator.

If you’re buying for the first time, you could be unsure as to what

a monthly mortgage payment should look like – use our calculator

to get a rough estimate.

Here's the process of applying for your first mortgage.

1

Get In touch on 07488 317183 or email mark@4wardmortgages.co.uk, or book an appointment, so we can discuss your circumstances and explain what information is required for us to start looking for the right mortgage.

2

Provide us with the documents needed and we will call to complete an in depth fact find to allow us to get your mortgage agreed in principle for the amount needed to secure your new home.

3

The exciting part! Start looking around for your new home safe in the knowledge that once you have found the property we have everything ready to apply for and secure a mortgage offer for you.

Frequently Asked Questions

Mortgages and protection can be confusing,

see the most commonly asked questions

and answers, to put your mind at rest.

Why life insurance is so important when you're a parent.

It goes without saying that raising children can be expensive, so your income, or that of another household member, is often the only way to pay for the everyday costs that come with looking after a child.

If you or someone you rely on were to pass away, it would take its toll financially, in addition to the emotional stress. Life insurance is one way to have a safety net in place.

Why life insurance is so important when you're moving home.

If you have life insurance, it’s a good idea to regularly review the cover to make sure it’s right for you and your current circumstances.

When you sign up for a policy, the extent of cover – how long it lasts, and how much it would pay out – is based on your financial situation and commitments at that time.

But these can change. Your life insurance policy needs to change as well to ensure your family is fully protected if the worst happens to you or your partner, so when moving home it’s important your cover still meets your needs.

Why life insurance is so important when taking out a new mortgage.

Mortgage life insurance can be used to help your loved ones pay off your mortgage if you die.

This type of life insurance is often sold as a decreasing-term policy so, as you gradually pay off your mortgage, your pay-out reduces over time. A mortgage life insurance claim typically pays out as a lump sum.

It’s designed to protect your loved ones if you die before your mortgage has been paid off. It will provide them with a lump sum so they can clear the mortgage debt and have one less financial burden at an already difficult time.